New Study Shows Markets Reward Policy Competence More Than Personal Popularity in U.S. Presidents

Research co-authored by Prof. Dr Nikolaos Antonakakis of the University of Nicosia, UNIC Athens, introduces a new Approval-Favorability Gap Index and finds that U.S. equity markets perform substantially better when presidents are perceived as more competent than personally popular

A new study published in Economics Letters introduces a novel high-frequency measure of political sentiment that separates what voters think about a president’s job performance from how they feel about the president personally. Co-authored by Prof. Dr Nikolaos Antonakakis of the University of Nicosia, UNIC Athens, and Prof. Dr Menbere Workie Tiruneh of the Webster Vienna Private University and the Slovak Academy of Sciences, the study shows that this distinction carries important information for financial markets.

Using 892 weekly observations across four U.S. presidencies from 2006 to 2026, the authors construct the Approval-Favorability Gap Index, or AFGI, which captures the difference between presidential favorability and job approval. The study finds that periods in which presidents are approved of more than they are liked are associated with markedly stronger stock market performance than periods in which presidents are personally liked more than they are approved of.

Why Approval and Favorability Are Not the Same Thing

Traditional presidential approval ratings combine two different public judgments: whether citizens believe a president is doing a good job and whether they personally like the individual. The study argues that these are psychologically and economically distinct. A president may be personally appealing but viewed as ineffective, or personally less popular but regarded as competent in policy terms.

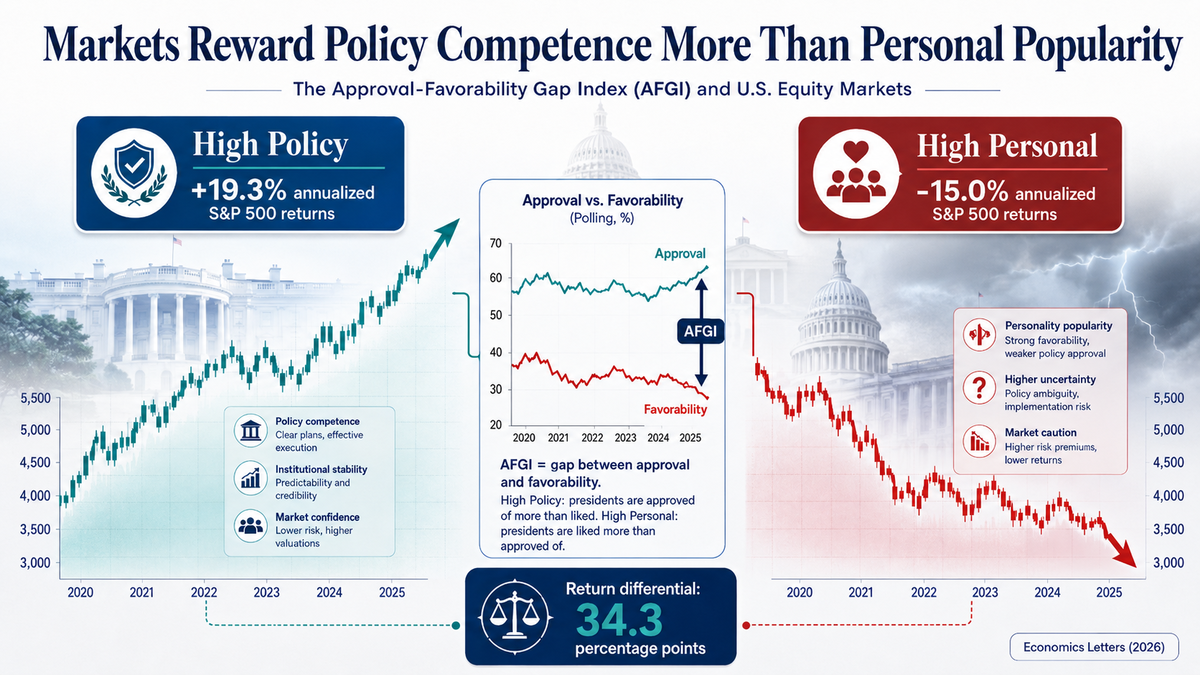

The AFGI is designed to capture precisely this gap. A positive AFGI indicates that favorability exceeds job approval, meaning the president is liked more than approved of. A negative AFGI indicates the opposite: the president is approved of more than liked. The authors then classify political environments into regimes such as “High Policy” and “High Personal” and examine how equity markets behave under each.

Markets Appear to Value Policy Credibility

The findings are striking. During “High Policy” regimes, when presidential job approval exceeds personal favorability, the S&P 500 recorded annualized excess returns of 19.3%. During “High Personal” regimes, when personal appeal exceeded perceived policy performance, annualized excess returns were -15.0%. This implies a 34.3 percentage point return differential between the two regimes.

The pattern remains significant after controlling for broader economic and financial conditions, including economic policy uncertainty, market volatility, recession indicators, and the CBOE Skewness Index. Across the full specification, the “High Policy” versus “High Personal” return differential remains statistically significant.

A “Popularity Discount” in Equity Markets

The study identifies what may be described as a “popularity discount”: periods when presidents are personally liked more than they are approved of are associated with weaker market performance and higher uncertainty. In contrast, periods in which presidents are perceived as more competent in policy terms are associated with stronger returns, lower volatility, and lower perceived tail risk.

The authors do not claim that the AFGI is a separately priced risk factor or that the relationship is causal. Rather, the index captures political environments in which systematic risk exposures and the equity risk premium differ. This distinction is important because it suggests that markets respond not only to political popularity, but also to the perceived credibility and competence of political leadership.

Researcher Comment

“Our results suggest that financial markets do not simply reward political popularity. They appear to place greater value on perceived policy competence. A president who is personally appealing but not regarded as effective may create a very different market environment from one who is less personally popular but viewed as capable of governing. This distinction matters because political sentiment is not one-dimensional. By separating approval from favorability, the AFGI provides a clearer lens through which to understand how markets price political risk.”

Prof. Dr Nikolaos Antonakakis

Department of Accounting, Economics and Finance

School of Business

University of Nicosia, UNIC Athens

Broader Implications

The study has implications beyond financial markets. By separating evaluative judgments from affective attitudes, the AFGI can be used to study legislative productivity, partisan consumer behavior, corporate political strategy, and the broader economic consequences of political leadership.

For investors, the findings suggest that headline popularity indicators may be insufficient. For policymakers, the results highlight the economic value of credible leadership. For researchers, the AFGI offers a parsimonious and high-frequency tool for studying political sentiment in a more nuanced way than traditional approval ratings allow.

About the Study

Title: The Approval-Favorability Gap Index and the Pricing of Political Risk: Policy Competence versus Personal Appeal in U.S. Equity Markets

Authors: Nikolaos Antonakakis and Menbere Workie Tiruneh

Journal: Economics Letters, Volume 264, 2026, Article 112953

DOI: https://doi.org/10.1016/j.econlet.2026.112953

Data: 892 weekly polling observations and 4,917 trading days covering U.S. presidencies from 2006 to 2026

Key Contribution: Introduction of the Approval-Favorability Gap Index, a new measure that distinguishes perceived policy competence from personal appeal in presidential opinion data.